Executive Summary

Redomestication is the legal process of transferring a company out of Wisconsin to another state, maintaining the existing federal employer identification number (FEIN), contracts, bank accounts, and in most cases, company name.

- No Downtime: When executed by a professional, there is no operational or financial disruption.

- Complexity: This process exists at the intersection of federal tax law and the laws of another state and Wisconsin. It is not a "DIY" weekend project.

- Timeline: Redomestication takes about three months from start to finish, and expedite options are available. The intake process is entirely electronic, takes less than five minutes to get started, and can be completed on our redomestication platform here.

- Credentials: All work is handled by a dually-licensed attorney and CPA.

- Pricing: Pricing varies depending on the size of the company and is flat-fee.

- Get Started: No need to "request a quote." The exact price can be seen in under 30 seconds at the above link.

Update July 2026: State legislatures are considering various legislative proposals that could change how a company is taxed in Wisconsin, including the possibility of new wealth, income, and capital gains taxes for the company and its owners. If you are considering relocating your company to another state, time is of the essence.

Several jurisdictions outside no-income-tax destination states are considering sweeping changes to state tax law which could result in a company and its owners paying tens of thousands, or in some cases, hundreds of thousands of dollars in new taxes. For a company considering redomesticating to another state, this should be at the forefront of any tax planning discussion. Redomestication, when coupled with a change of residency to another state and a reduction or cessation of business activity in Wisconsin, can be an effective way to reduce or eliminate tax nexus in Wisconsin, thereby yielding lower taxes for the company and its owners. Ask your CPA for more information.

Table of Contents

- The Redomestication Process in a Nuthsell

- Requirements to Transfer a company from Wisconsin to another state in 2026

- Why hire Cummings & Cummings Law to transfer your company from Wisconsin to another state?

- Legal requirements for moving your company to another state (updated July 2026)

- The sequence of moving a company to another state from Wisconsin

- How long does it take to move a company from Wisconsin to another state?

- How much does it cost to transfer a company from Wisconsin to another state?

- Tax considerations when moving a company from Wisconsin to another state (updated July 2026)

- Specific requirements to transfer a company to another state from Wisconsin

- Redomestication vs. Foreign Registration vs. Merger vs. Dissolution: A Comparison

- Frequently asked questions: moving a company to another state from Wisconsin

- Common misconceptions about redomestication

The Redomestication Process in a Nutshell

1. Enter your biz name on our portal here.

Then click "get exact price" and follow the steps.

Takes less than five minutes to start, and then our attorneys get to work.

Submit payment securely online then sit back and relax.

2. We prepare the legal docs.

Our dually-licensed attorney+CPA prepares the legal documents and sends them to you via DocuSign.

You sign. We take it from there.

3. We submit the legal filings to the states.

We monitor the status closely, respond to inquiries from their offices, and send you weekly updates.

No extra charge. 100% success rate.

4. Approved! ✅

We send you a checklist of go-forward obligations and simple steps for your tax pro to follow.

120% money-back guarantee if we do not succeed.

Still have questions? Schedule a meeting with our attorney and CPA.

Redomestication, also known as redomesticating, refers to the lesser-known legal process of transferring or moving the "home state" of an existing corporation, partnership, or LLC to a new state. It means keeping your existing company name, credit, and federal employer identification number (FEIN) without wasting time and money creating a new business entity, applying for foreign registration, or moving assets between companies.

— Prof. Chad D. Cummings, Esq., CPA

Click Here to Start Your Redomestication Now

Requirements to Transfer a company from Wisconsin to another state in 2026

Overview: how redomestication works

Welcome to the complete guide for moving your company from Wisconsin to another state presented by Cummings & Cummings Law, a Florida and Texas law firm focused on the legal process of redomestication.

Moving your company from Wisconsin to another state can offer significant advantages, particularly if you're seeking a more favorable tax environment or streamlined business regulations. No-state-income-tax destination states are known for their business-friendly policies, which can lead to substantial savings for your company. Before initiating the process, it's essential to evaluate your current setup in Wisconsin and ensure compliance with both states' requirements to avoid any legal pitfalls.

The redomestication process typically involves filing specific documents with the secretaries of state in both Wisconsin and the destination state. This includes preparing a plan of redomestication, obtaining board and shareholder approvals if applicable, and submitting articles of redomestication in the destination state. Unlike simply registering as a foreign entity, this method allows your company to fully transition its domicile, shedding ongoing obligations in Wisconsin while retaining your federal EIN and business continuity.

Once approved, your company will operate under the destination state's laws, potentially benefiting from asset protection and operational flexibility unique to the state. However, consulting with legal and tax professionals familiar with both Wisconsin and the destination state is crucial to navigate any nuances, such as franchise taxes or entity conversion rules. This strategic move can position your company for long-term growth in a more supportive jurisdiction.

Why hire Cummings & Cummings Law to transfer your company out of Wisconsin?

Cummings & Cummings Law is a dually-licensed Florida and Texas attorney and Certified Public Accountant practice that has completed more than 500 redomestications with a 100% success rate and a 120% money-back guarantee. Our firm prepares the Plan of Conversion, files the Wisconsin outbound instrument (or its functional equivalent under Wisconsin law), coordinates with the destination state of your choice, and provides weekly status updates at no additional charge.

The attorney relationship imposes fiduciary duties that services like LegalZoom® and RocketLawyer® do not owe. As Justice Benjamin Cardozo wrote in Wendt v. Fischer (1926), a fiduciary “is held to something stricter than the morals of the market place. Not honesty alone, but the punctilio of an honor the most sensitive, is then the standard of behavior.” A non-attorney performing the work of an attorney is practicing law without a license, which is a crime in every state.

Our pricing is flat-fee, our typical timeline is two to three months from engagement to acceptance by both states (expedite options available), and the same attorney and CPA who signs the filings performs the work. No part of the engagement is delegated to apprentices, assistants, or third-party vendors. Every situation is different. The information on this page is general and does not constitute legal or tax advice. Speak with your existing tax preparer before proceeding so that he or she can identify any state-tax or federal-tax considerations specific to your facts.

Federal legal authority for moving your company out of Wisconsin (updated July 2026)

An outbound redomestication out of Wisconsin is governed by the redomestication statutes of Wisconsin (cited below in the section specific to your state) together with the federal tax-free reorganization provisions at Sections 351, 355, and 368(a) of the Internal Revenue Code and applicable Treasury Regulations. The federal F-reorganization framework under I.R.C. § 368(a)(1)(F) and Treas. Reg. § 1.368-2(m) allows a properly-structured redomestication to be a non-taxable event at both the entity and owner levels.

Few legal transactions implicate such a broad cross-section of state and federal law. Laws updated in 2026 present hidden landmines for inexperienced attorneys and do-it-yourself filers alike. The federal tax-free treatment of a redomestication depends on strict compliance with the statutory requirements of both Wisconsin and the destination state. A defective filing can convert a non-taxable continuity transaction into a taxable dissolution-and-reformation.

Among other things, an outbound redomestication out of Wisconsin requires the preparation and execution of a Plan of Conversion (or, in some states, a Plan of Domestication, Plan of Transfer, or Declaration of Conversion) approved by the requisite vote of the owners; board meeting minutes or unanimous written consent ratifying the Plan; the outbound filing instrument with the Wisconsin Secretary of State (or its equivalent agency); the inbound filing instrument with the destination state; and final tax returns with the Wisconsin Department of Revenue (or equivalent) where applicable. Each step is jurisdiction-specific. The Wisconsin statutes governing each step are summarized in the state-specific section below.

The sequence of moving a company out of Wisconsin

Timing is everything. There is a strict, mandatory sequence which must be observed when transferring a company out of Wisconsin. Proceeding out of order will result in the inadvertent termination of the company, which may be a taxable event, the formation of a duplicate company (which creates serious tax headaches), or the devolution of the liabilities of the company to its owners. This is lawyer-speak meaning that, if not performed correctly and sequentially, the liabilities (known, unknown, past, present, and future) of the company may become the personal obligations of the owners, potentially resulting in bankruptcy and financial ruin.

The general sequence is as follows:

- First, a legal Plan of Conversion is drafted and submitted to the owners of the company;

- Second, the owners discuss and vote upon the Plan of Conversion, either at a properly-called meeting or via a unanimous written consent;

- Third, the inbound filing instruments are filed with the destination state's Secretary of State (or equivalent) and subject to that state's review and approval period;

- Fourth, only after the destination state approves the redomestication, the Wisconsin outbound filing instrument is filed with the Wisconsin Secretary of State (or equivalent agency), subject to that state's review and approval period.

How long does it take to move a company out of Wisconsin?

An experienced attorney can prepare documents within 48 to 72 hours of engagement. The destination state's review period varies by jurisdiction and typically ranges from two days (expedited) to eight weeks (standard mail processing). The Wisconsin outbound filing review period adds an additional two to eight weeks depending on the processing backlog at Wisconsin. The entire process generally requires two to three months from engagement to final acceptance by both states. With expedite at both ends, the timeline can be compressed to three to four weeks.

How much does it cost to transfer a company out of Wisconsin?

Professional fees for redomesticating a single-owner company start just under $2,000, plus the state-imposed filing costs of Wisconsin (set forth in the section below) and the state-imposed filing costs of the destination state of your choice. Our most updated pricing can be viewed here: costs to move a company out of Wisconsin, where the intake process can be completed in under five minutes, and then our attorneys get to work. Our firm charges a flat-fee for redomestications of any company with five owners or fewer; a single-owner company should expect to pay less than a multi-owner entity.

By comparison, a traditional merger may cost $20,000 or more, dissolution can reach five or six figures, and fixing a failed or incomplete redomestication routinely exceeds $15,000 and in some cases cannot be fixed at all. Online filing services may charge less, but they often prepare and file documents incorrectly and may be practicing law without a license, which is a crime in every state.

If your company has complex structures or ongoing operations tied to Wisconsin, consider the timeline—approvals can take several weeks to months.

Ultimately, relocating to another state via redomestication empowers business owners to optimize their setup without the hassle of dissolving and reforming the entity anew.

Tax considerations when moving a company from Wisconsin to another state (updated July 2026)

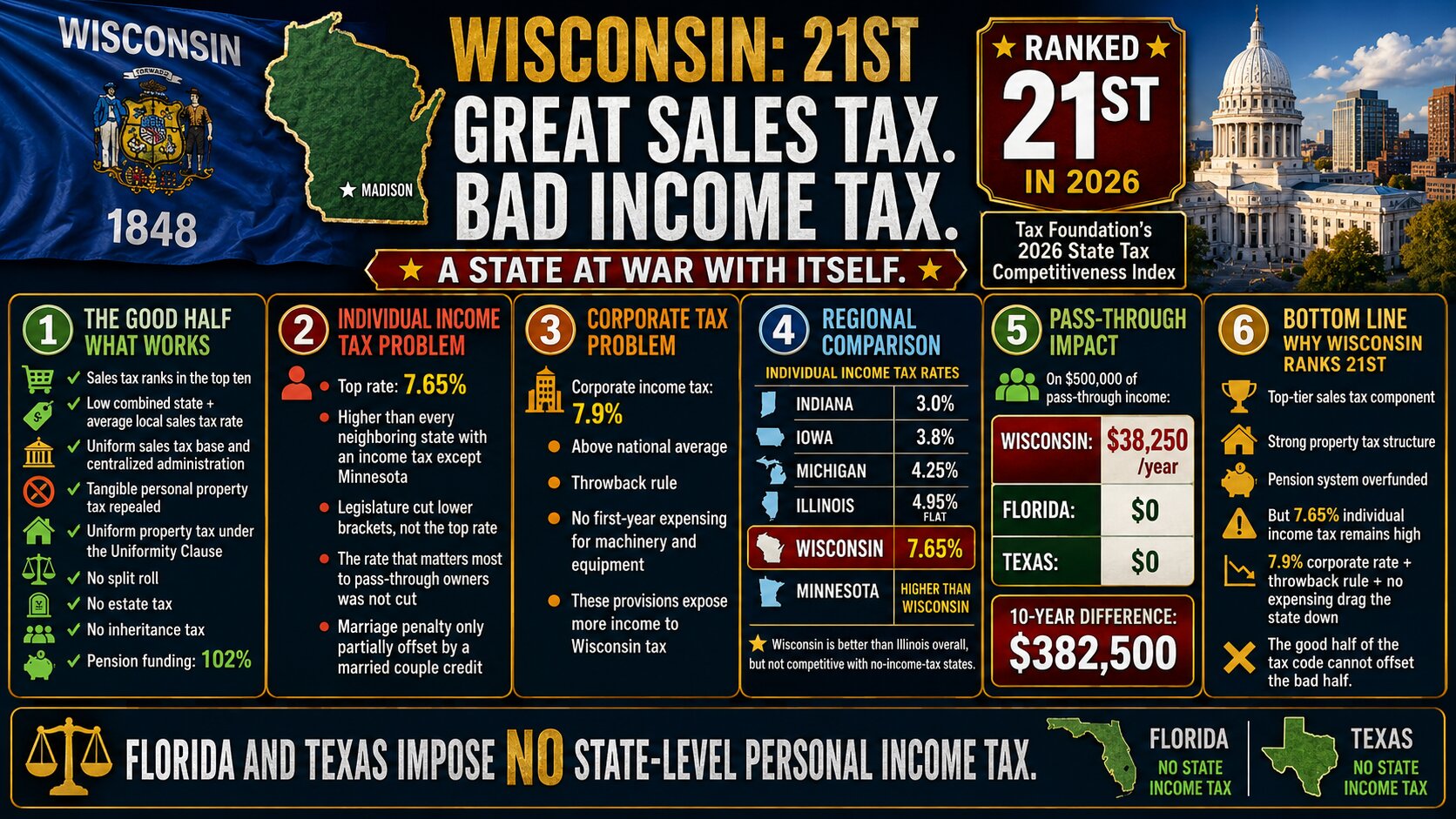

Wisconsin imposes a graduated individual income tax with rates reaching 7.65 percent. Wisconsin also imposes a 7.90 percent corporate income/franchise tax, one of the higher corporate rates in the nation. Pass-through entities are not taxed at the entity level. Wisconsin ranks 21st on the Tax Foundation's 2026 State Tax Competitiveness Index. More information is available from the Tax Foundation and the Wisconsin Department of Revenue.

Wisconsin imposes a 5.00 percent state sales tax. When combined with local taxes averaging 0.72 percent, the combined state and local rate is 5.72 percent, ranking 42nd in the nation. Wisconsin does not impose a state-level estate tax or inheritance tax. For owners of a company redomesticating from Wisconsin to another state, Wisconsin's top individual income tax rate of 7.65 percent and its corporate income/franchise tax rate of 7.90 percent are both above the national average. The combined sales tax rate is low, which provides partial offset, but the income and corporate tax rates are the primary drivers of the tax burden for business owners. The ranking of 21st on the Tax Foundation Index reflects the balance of a low sales tax against above-average income and corporate rates.

Specific requirements to transfer a company to another state from Wisconsin

Moving a company from Wisconsin to another state is entirely possible, but Wisconsin has specific laws that must be strictly followed, and the process varies from other jurisdictions.

Many business owners are wrongly told that it is impossible or impractical to transfer a company out of Wisconsin, but that is simply false. There are three primary reasons for this misinformation:

- first, many attorneys are unaware of the statutory authority for Wisconsin redomestications;

- second, Wisconsin uses different terminology which hinders understanding; and

- third, Wisconsin law requires the preparation of a legal Plan of Conversion, which online filing services cannot prepare (and as a result, these services will instead tell their customers that it is impossible to transfer a company out of Wisconsin, which is patently false).

Unique requirements to move a company to another state from Wisconsin

Here are the Wisconsin-specific factors to consider when moving a company to another state after the attorney-prepared Plan of Conversion has been adopted by board meeting minutes or a unanimous written consent and the destination state's Secretary of State has approved the redomestication:

- Wisconsin uses the term conversion to refer to redomestications and requires the filing of a Statement of Conversion with the Wisconsin Department of Financial Institutions, governed by the Wisconsin Uniform Limited Liability Company Law, Wis. Stat. § 183.1041 et seq.

- Before filing, the entity must adopt a Plan of Domestication (Wisconsin uses this terminology for the internal governance document even under its conversion statute) approved by the requisite vote of the owners under Wisconsin law, specifying the terms and conditions of the redomestication and the treatment of membership interests.

- Wisconsin requires the entity to be in good standing and current on all annual report filings before the redomestication filing will be accepted; the entity should also address Wisconsin state tax obligations with the Wisconsin Department of Revenue.

- The Wisconsin state filing costs to redomesticate out of Wisconsin are $294, in addition to the destination state filing costs. These costs are exclusive of legal fees.

- Contrary to popular belief, a certificate of good standing from Wisconsin is not required to complete the redomestication, though the entity must be in good standing with the Wisconsin Department of Financial Institutions at the time of filing.

- Wisconsin filings are made with the Department of Financial Institutions (DFI), not a Secretary of State. DFI has its own filing procedures and formatting requirements, and correspondence should be directed to DFI's Division of Corporate and Consumer Services to avoid misdirection.

- Wisconsin's use of the term "Plan of Domestication" for the internal governance document despite using the term "conversion" for the filed instrument creates a terminological mismatch that can be confusing. The entity should use "Statement of Conversion" for the filing instrument and "Plan of Domestication" for the internal document to match Wisconsin statutory usage.

- Under Wisconsin law, the converted entity is the same entity that existed before the conversion, and all property, rights, and obligations continue unimpaired.

- The entity should coordinate with its tax professional to file final Wisconsin returns and close any open accounts with the Wisconsin Department of Revenue.

- A bespoke cover letter explaining the nature of the transaction, enclosures, and state filing costs is also recommended to facilitate processing.

Illustrative Scenario: Moving a Company Out of Wisconsin

A two-shareholder S corporation in Milwaukee, Wisconsin, with $525,000 in pass-through distributions faced Wisconsin's 7.65 percent top individual rate. After both shareholders relocated to Florida and the company redomesticated, the owners eliminated approximately $40,100 in annual Wisconsin tax exposure.

Illustrative scenario only; not based on an actual client; past results do not guarantee future outcomes. Every situation is different. The figures above are based on stylized assumptions and do not reflect the facts of any particular taxpayer. Speak with your existing tax preparer before proceeding so that he or she can identify any state-tax or federal-tax considerations specific to your facts. Our firm does not render tax advice on this page; tax-return preparation and tax-controversy work are separate engagements at additional charge.

Click Here to Start Your Redomestication Now

Redomestication vs. Foreign Registration vs. Merger vs. Dissolution: A Comparison

Redomestication is a distinct legal process from foreign entity registration, merger, or dissolution.

Redomestication is generally the most efficient and cost-effective method for relocating a business to a new state, particularly when the company has permanently ceased operations in its original state. It does not involve dissolution. Many people make the mistake of dissolving their company when relying on incomplete or misleading advice.

Unlike foreign entity registration or merger, redomestication allows a business to retain its EIN, contracts, credit history, and brand identity—preserving continuity while minimizing tax risks and administrative burdens. It also eliminates the need to maintain dual registrations and tax obligations, potentially saving substantial time and money. By contrast, foreign registration can create ongoing compliance costs in the former state, and mergers often involve unnecessary legal complexity and higher fees.

Redomestication is, in many circumstances, far preferable to registering an LLC or corporation as a foreign entity, especially where the LLC or corporation has permanently moved its operations and will not be returning to the prior state in the near future.

Some attorneys, unfortunately, confuse their clients by recommending a foreign entity registration in the new state, or worse, a merger, where a redomestication would have accomplished the goals of moving their business to a new state efficiently and effectively.

The top seven benefits of moving your company (LLC, corporation, or partnership) to a new state via redomestication to transfer your business include:

- Maintaining your existing federal employer identification number, eliminating the tax headaches of forming a new company or transferring assets between companies (and inadvertently triggering a hefty tax bill from the IRS) when you move your business to a new state;

- Keeping your existing business credit history and track record, safeguarding your reputation with clients, vendors, and creditors when moving your LLC or corporation to a new state;

- Continuing your existing business name (in almost every case), protecting your most important assets when moving your company to a new state: your brand, reputation, and time you have already invested in search engine optimization;

- Maintaining your existing contracts with customers and vendors because moving your business to a new state via redomestication does not create a new company: it maintains your existing company, saving you dozens (or even hundreds) of hours re-writing (and re-negotiating) contracts and changing banks;

- Eliminating the need to continue paying registration fees and taxes in your prior state (assuming you have discontinued your operations there and have permanently relocated to a new state), potentially saving you tens of thousands of dollars (or more) in state taxes every quarter when you move your business to a new state;

- Avoiding unnecessary IRS scrutiny because moving your LLC or corporation to a new state via redomestication is a tax-free transaction under the Internal Revenue Code; and

- Reducing the amount of time you spend on administrative filings, saving you untold hours annually, by moving your company to a new state.

Before taking the "penny wise and pound foolish" approach of foreign entity registration or spending countless hours and exorbitant legal fees (and possibly taxes) on a merger or merger-gone-wrong to move your company to a new state, ensure you understand your options.

| Redomesticate | Foreign Entity | Merge | Dissolve | |

|---|---|---|---|---|

| Need to Continue Paying & Filing Registration Renewals in Former State | ✅ No | ❌ Yes | ⚠️ Varies | ☠️ No, she's dead, Jim. |

| Stop Paying Taxes in the Former State* | ✅ Yes | ❌ No | ⚠️ Varies | ☠️ Tax event.* |

| Initial Complexity | ✅ Low | ⚠️ Varies | ❌ High | ❌ High, when done right. |

| Ongoing Complexity | ✅ Very Low | ❌ High | ❌ High | ☠️ None. All gone. |

| Initial State Filing Costs | ✅ Low | ⚠️ Varies | ❌ High | ⚠️ Varies |

| Timing | ✅ Fast | ⚠️ Varies | ❌ Slow | ⚠️ Varies |

| Legal Fees | ✅ Low | ⚠️ Varies | ❌ $10,000 or more | 🔥 Very high to fix. |

| *While every situation is different and dependent upon tax nexus, redomesticating can be an effective way to reduce or eliminate taxes in a former state in certain circumstances. Ask your CPA for more information. Our firm does not provide tax advice or perform tax work except by separate engagement at an additional charge. | ||||

In most circumstances, redomestication (and not a foreign entity registration or costly and complicated merger) is the best route to achieve a change in company domicile to a new state.

Why is redomestication the superior option to move a company from Wisconsin to another state?

Redomestication keeps the business alive while moving its legal home to another state, which can allow the business to stop paying and filing annual registration renewals in Wisconsin if it has ceased operations there. The tax outcome depends on the facts and tax nexus, but the result is often that the redomesticated company has no remaining connection to Wisconsin, which can reduce or eliminate Wisconsin tax exposure.

Why is foreign entity registration inferior to redomestication when moving a company from Wisconsin to another state?

Foreign entity registration keeps the company domiciled in Wisconsin and registers it to do business in the destination state, which means continuing to pay and file renewals and taxes in Wisconsin. The business now manages two or more state compliance tracks, increasing the chance that a missed renewal, registered agent change, or notice triggers penalties, loss of good standing, or disputes with banks and regulators.

Why is a traditional merger usually the wrong way to move a company from Wisconsin to another state?

A traditional merger is a slower, higher-complexity path with legal fees that can reach $10,000 or more, and six or seven figures for complex transactions. When performed incorrectly, a merger may be a taxable event. The merger process also creates follow-on work: re-titling assets, harmonizing governing documents, novating and re-negotiating existing contracts, establishing new bank accounts, and repairing overlooked items that can surface years later. A single missed consent or broken assignment clause can convert a planned administrative exercise into a dispute or business interruption.

Why is dissolution the wrong way to move a company to another state from Wisconsin?

Dissolution kills the company. There is nothing left to move. Even if you think your company is dormant, breaches of contract, tax liabilities, and other claims may not surface until years down the road. If the company is dissolved, those claims may subject your personal assets to unlimited personal liability because the veil of protection for your company no longer exists. Dissolution can also trigger a taxable event under the Internal Revenue Code and the laws of Wisconsin. Redomestication, when performed by a competent attorney, is a non-taxable event.

Unless you are closing your doors and going out of business, dissolution should not enter the equation. If other professionals are suggesting dissolution, seek a second opinion. If you dissolve your company, you are not moving it; you are pulling the plug.

Click Here to Start Your Redomestication Now

Frequently asked questions: moving a company to another state from Wisconsin

Below are some of the most commonly asked questions our firm receives from business owners interested in transferring their company to another state from Wisconsin, prepared by a dually-licensed Florida and Texas attorney and Certified Public Accountant.

-

1. What is redomestication?

Redomestication is the statutory conversion of a company from Wisconsin to another state under the destination state's conversion statute. The company retains its Federal Employer Identification Number, contracts, bank accounts, credit history, and legal continuity. No new entity is formed and no assets transfer.

Redomestication is the process of legally transferring a company's home state from Wisconsin to another state. The company retains its existing name, credit history, contracts, bank accounts, and federal employer identification number (FEIN) without creating a new entity, transferring assets, triggering federal income tax, applying for foreign registration, or dissolving the original company.

The company that exists after the redomestication is the same legal entity that existed before. It carries forward all prior history, rights, obligations, and liabilities as a matter of law. The process is authorized under the applicable statutes of both Wisconsin and the destination state.

-

2. How does redomestication differ from foreign qualification or merger?

Foreign qualification registers the company in the destination state while preserving Wisconsin domicile, requiring dual-state compliance. Merger forms a new destination-state entity and dissolves the old, requiring asset transfers and a new Federal Employer Identification Number. Redomestication changes domicile only, preserving the same legal entity by operation of the destination state's conversion statute.

Business owners who wish to operate in the destination state often encounter three distinct legal mechanisms:

- Foreign Qualification: The company registers in the destination state while remaining domiciled in Wisconsin, requiring ongoing compliance and fees in both states.

- Merger: A new company is formed in the destination state and the original merges into it. This can trigger tax consequences and requires transferring contracts, bank accounts, and assets to the surviving entity.

- Redomestication: The company itself changes domicile from Wisconsin to another state. No new entity is created. The FEIN, contracts, bank accounts, and credit history remain intact.

Redomestication is, in most cases, the superior approach because it preserves continuity, avoids duplicate entities, and minimizes administrative and tax burdens.

-

3. How much does redomestication cost?

The flat-fee covers attorney and Certified Public Accountant work from intake through final acceptance and includes the custom Plan of Conversion required by the destination state's conversion statute. State filing costs vary by jurisdiction; Wisconsin filing costs apply for the exit instrument and the destination state filing costs apply for the conversion document.

For a one-time flat-fee plus state filing costs, our dually-licensed attorney and CPA prepares and files all required legal instruments to change the domicile of your company from Wisconsin to another state. The flat-fee covers the entire process from initial consultation through final confirmation of acceptance but excludes tax work.

Many online services and some attorneys omit the preparation of a custom Plan of Conversion, which can result in a failure of the process and unforeseen tax and legal complications. We know of no other service that will perform all of these legal services to transfer your company to another state from Wisconsin at this competitive price.

-

4. Why should I transfer my business to another state?

State-level tax treatment, asset protection statutes, regulatory environment, and proximity to operations are the most common drivers for relocating a company from Wisconsin to another state. Owners should evaluate the destination state's tax code, registered-agent rules, and annual filing burden before electing a domicile change.

States such as Florida and Texas impose no state-level personal income tax. Most company types, including LLCs, S corporations, and partnerships, pay no state-level income tax or franchise tax. Such destination states also offer strong asset protection statutes, a large consumer market, and well-developed infrastructure for business formation and compliance. Owners of pass-through entities who relocate to a no-income-tax destination state may realize meaningful tax savings at the state level.

-

5. What are the federal income tax implications of redomesticating?

A redomestication of a company from Wisconsin to another state that satisfies Treasury requirements qualifies as a tax-free F-reorganization under I.R.C. § 368(a)(1)(F). Tax attributes carry over under I.R.C. § 381. No gain or loss is recognized at the entity or owner level. The Internal Revenue Service confirmed this treatment in Rev. Rul. 2008-18, 2008-13 I.R.B. 674.

Redomestication is a form of non-taxable business reorganization recognized under Sections 351, 355, and/or 368(a) of the Internal Revenue Code (IRC) and applicable Treasury Regulations. When executed in compliance with the statutory requirements, transferring your company from Wisconsin to another state using this approach will not trigger any new federal income taxes at either the company or owner level.

The tax-free treatment arises because the redomestication is a change in domicile only, not a sale, exchange, or distribution of assets. The company's tax attributes, including its basis in assets, carry forward without adjustment or new accounting.

You will need to apprise the IRS of your new business address. Our firm can handle this administrative task for you at a nominal, additional charge.

Important: The tax-free treatment of a redomestication depends upon strict compliance with all applicable requirements. Failure to prepare and adopt a proper Plan of Conversion, or failure to file the required instruments with both Wisconsin and the destination state, can jeopardize the non-taxable character of the transaction. This is one of several reasons why the Plan of Conversion, prepared by a competent Florida and Texas attorney and CPA, is an essential component of the process. -

6. How does the redomestication process work?

The client submits the online intake and payment. The attorney drafts a custom Plan of Conversion under the destination state's conversion statute. The conversion document is filed with the destination state's Secretary of State. After acceptance, the corresponding statement of conversion is filed with the Wisconsin Secretary of State under the Wisconsin conversion statute (Wis. Stat. § 183.1207 et seq.) to terminate Wisconsin domicile.

The process proceeds in six steps: (1) complete the intake workflow on our website and submit payment; (2) our attorney prepares a custom Plan of Conversion, provided to you for review and signature via DocuSign; (3) our firm files documents with the destination state's Secretary of State; (4) upon acceptance, we provide you with filed and stamped documents; (5) our attorney files a statement of conversion with Wisconsin, completing the redomestication; (6) we provide guidance on next steps and ongoing destination-state filing requirements.

Most online services and some attorneys omit Step 2 (the Plan of Conversion) and Step 5 (the filing with Wisconsin). These omissions can result in a failure of the process and unforeseen complications which may not be remediable.

-

7. What is a Plan of Conversion, and why is it important?

A Plan of Conversion is the legal instrument required by the destination state's conversion statute that authorizes the change of domicile. It must identify the converting entity, the destination jurisdiction, and the treatment of ownership interests. Omission causes filing rejection by the destination state's Secretary of State and may forfeit federal tax-free treatment under I.R.C. § 368(a)(1)(F).

A Plan of Conversion is the foundational legal document that authorizes and governs the redomestication. Both Wisconsin and the destination state law require its adoption as a prerequisite to filing. It sets forth the terms of the conversion, identifies the jurisdictions, and specifies the treatment of ownership interests. Failure to prepare and adopt a proper Plan of Conversion can result in rejection of the filing, a defective conversion, loss of the non-taxable character of the transaction, disputes among owners, and personal liability for those who authorized a defective transaction.

Our attorney prepares a custom Plan of Conversion for every engagement. It is not a template or boilerplate form.

-

8. How long does the redomestication process take?

Two to three months from engagement is typical, governed by the processing times of the destination state and Wisconsin filing offices. Many destination states offer expedited processing for an additional fee, reducing the destination-state portion to several business days. Cummings & Cummings Law provides weekly status updates throughout the engagement.

The process typically takes two to three months from the date of engagement. The principal variable is the turnaround time of the destination state's Secretary of State and Wisconsin. When expediting is available, we can compress the timeline to less than a month. We provide weekly status updates throughout the process at no additional charge.

Click Here to Start Your Redomestication Now

Common misconceptions about redomestication

Below are some of the most common misconceptions our firm encounters when advising business owners on transferring their company from Wisconsin to another state.

-

1. "I need to form a new company in the destination state and dissolve the old one in Wisconsin."

Verdict: False. Statutory conversion under the destination state's conversion statute changes the company's domicile from Wisconsin to another state without creating a new entity or dissolving the existing one. The converted entity is, by statute, the same legal entity that existed before. The Federal Employer Identification Number, contracts, and credit history carry forward without interruption.

Incorrect. Redomestication changes the company's state of domicile without creating a new entity or dissolving the existing one. The company that exists after the conversion is the same legal entity that existed before. Its FEIN, contracts, bank accounts, and legal history remain intact. Forming a new entity and dissolving the old one can trigger tax consequences, require asset transfers, and disrupt existing contractual relationships.

-

2. "Changing my company's state of domicile will trigger federal income tax."

Verdict: False. A redomestication of a company from Wisconsin to another state that satisfies Treasury requirements qualifies as a tax-free F-reorganization under I.R.C. § 368(a)(1)(F), with attribute carryover under I.R.C. § 381. The Internal Revenue Service confirmed this treatment in Rev. Rul. 2008-18, 2008-13 I.R.B. 674. Strict statutory compliance is required.

When executed in compliance with the applicable statutory requirements, redomestication is a non-taxable reorganization under the federal Internal Revenue Code and Treasury Regulations. No gain or loss is recognized at the entity or owner level. The company's tax attributes, including its basis in assets, carry forward without adjustment. The critical condition is strict compliance: the company must adopt a proper Plan of Conversion, file the required instruments with both Wisconsin and the destination state's Secretary of State, and satisfy all procedural requirements of both jurisdictions.

-

3. "A Plan of Conversion is optional or just a formality."

Verdict: False. the destination state's conversion statute requires a Plan of Conversion identifying the converting company, the destination jurisdiction, and the treatment of ownership interests as a statutory prerequisite to filing the conversion document. Omission causes filing rejection by the destination state's Secretary of State and may forfeit federal tax-free treatment under I.R.C. § 368(a)(1)(F).

The laws of both Wisconsin and the destination state require the adoption of a Plan of Conversion as a prerequisite to filing. Omitting this document can result in rejection of the filing, a defective redomestication that may not be recognized as legally effective, and loss of the non-taxable character of the transaction under federal tax law. Many online filing services and some attorneys omit this step, which is one of the most common causes of failed conversions and future litigation.

-

4. "I only need to file paperwork with the destination state's Secretary of State to complete the conversion, and I can find a template online."

Verdict: False. A complete redomestication requires the conversion document filed in the destination state under the destination state's conversion statute plus a corresponding statement of conversion filed in Wisconsin under the Wisconsin conversion statute (Wis. Stat. § 183.1207 et seq.) to terminate Wisconsin domicile. Filing only with the destination state leaves the company with dual domicile and continued Wisconsin filing and tax obligations.

A complete redomestication requires filings with both the destination state's Secretary of State and Wisconsin. Failing to file with Wisconsin can leave the company in a state of dual domicile, resulting in continued filing obligations, annual report requirements, and tax assessments in Wisconsin. The fill-in-the-blank templates found online are not specific to redomestication and may result in the unintentional termination of your company.

-

5. "My company will require a new FEIN after the redomestication."

Verdict: False. The Federal Employer Identification Number of the company carries over from Wisconsin to another state because the converted entity is the same taxpayer under I.R.C. § 368(a)(1)(F) and Treas. Reg. § 301.6109-1. The Internal Revenue Service confirmed this treatment in Rev. Rul. 73-526, 1973-2 C.B. 404 (Situation 3); Rev. Rul. 64-250, 1964-2 C.B. 333; and Rev. Rul. 2008-18, 2008-13 I.R.B. 674.

The company's federal employer identification number (FEIN) does not change as a result of redomestication. The IRS treats the converted company as the same taxpayer before and after the conversion. See I.R.C. § 368(a); Rev. Rul. 73-526, 1973-2 C.B. 404 (Situation 3); Rev. Rul. 64-250, 1964-2 C.B. 333; Rev. Rul. 2008-18, 2008-13 I.R.B. 674. A new FEIN would be required only if the company were dissolved and a new entity formed, or in the case of a traditional merger, which is not what occurs in a redomestication.

Click Here to Start Your Redomestication Now